Critical, Not Connected: The Real State of SMRs

Two things happened this week worth discussing when it comes to new nuclear deployment.

First: Bloomberg Intelligence now projects a 60%+ jump in U.S. nuclear capacity by 2050, driven almost entirely by AI and data-center demand. Not some distant climate goal, but real grid pressure right now. That’s a major bump from earlier, more tepid forecasts, and it moves nuclear from “someday” into “this decade.”

Second: Yesterday, DOE announced its new Reactor Pilot Program, selecting 10 companies—Oklo, Last Energy, Terrestrial Energy, and others—to fast-track small and advanced reactors, with several aiming for achieving criticality by mid-2026.

Why the Spotlight Is on SMRs

For the last 15 years, U.S. electricity demand was basically a flat line — less than 0.5% annual growth. That meant utilities had zero incentive to gamble on new nuclear. Gas was cheap, solar was subsidized, and efficiency gains kept consumption stable.

Then AI and data centers walked in and tore up the charts.

Data center demand is set to triple by 2030 — from 4% of U.S. electricity use to as much as 12% (see linked McKinsey report)

FERC projections now show over 5% annual growth for the next decade, with nearly 38 GW of new peak demand needed by 2028 — check out this report by Grid Strategies for a detailed breakdown. One caveat — this report is from 2023. Last year, the projections by the World Resources Institute surged to over 120 GW by 2029! That 5-fold increase in the projection alone over just two years (2022 to 2024). The lesson? We are probably not even close to estimating the actual demand in energy by 2030.

Translation: the grid is about to get crushed.

Enter SMRs. Suddenly, the pitch — “modular, local, factory-built nuclear power” — looks like a silver bullet for politicians desperate to avoid brownouts and data center CEOs who want to virtue-signal carbon neutrality.

The reality? Most SMRs are scaled-down versions of reactor designs we’ve previously built. They still split atoms, still make steam, and still produce nuclear waste. What’s new is the manufacturing approach—assembling core systems in a factory and shipping them to the site—which promises faster deployment and potentially lower costs… if we get to the mass-production stage.

How They Work and What’s Different

The core – uranium (sometimes you hear plutonium or even thorium) fuel undergoes fission, releasing heat.

Heat transfer – water, gas, sodium, lead or molten salt moves that heat to a turbine system.

Power conversion – steam or gas spins a generator to produce electricity.

Safety – many designs use passive safety systems (gravity-fed coolant, natural circulation) to prevent accidents without active pumping.

Modules typically produce 50–300 MWe, enough for tens of thousands of homes or one very large AI campus.

The Problem With Betting Everything on SMRs

The same obstacles that have dogged large nuclear haven’t magically disappeared:

Cost per megawatt is still high until you have a real manufacturing line pumping out dozens of units.

Fuel supply chain, especially HALEU, that’s required by many SMRs, is a bottleneck. Russia is currently the world’s largest producer. That’s… awkward. Let’s see where the Anchorage meeting goes today.

Waste doesn’t magically vanish since SMRs also generate high-level and low-level waste as large plants, sometimes more per MWh. Some claim to burn waste. Let’s pause on discussing this claim since we do not have a good national strategy on how to implement that.

Regulation still exists. Yes, DOE’s test reactor program might bypass some NRC steps, but any grid-connected unit will need full licensing.

Why a Hybrid Strategy Makes More Sense

If you need to keep the lights on in a growing city or power-hungry industrial hub this decade, you build big reactors now. They’re proven, licensable, and can deliver the gigawatts you need without playing supply chain roulette. But, the supply chain is still an issue. These reactors require components that are not easy to source. For example, pressure vessels (very heavy forgings produced in one piece) are manufactured in four countries: Japan (Japan Steel Works), China (China First Heavy Industries, China Erzhong, SEC), France (Le Creusot), and Russia (OMZ Izhora). Nothing domestically approaches the capabilities needed for this type of production.

Meanwhile, you keep SMRs in development refining designs, building HALEU production, and stress-testing modular manufacturing. When they’re ready, they’ll fit perfectly into niche and emerging markets:

Remote or island grids

Data centers and industrial parks that want dedicated baseload

Areas where political or physical constraints make large plants impossible

Times when it’s cheaper to invest in SMRs with domestic production of critical components rather than working abroad to manufacture vessels, heat exchangers etc.

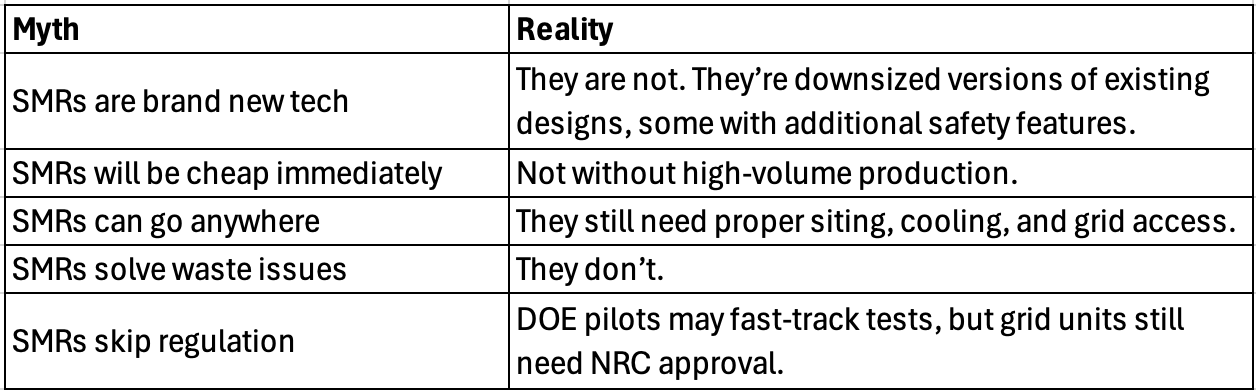

Myths vs. Reality

Criticality vs. Operation and Why It Matters

In the DOE pilot announcement, the goal is reactor criticality, not full commercial operation. That distinction matters because people outside the field often think “critical” means “running and sending power to the grid.” It doesn’t.

Criticality

Definition: The reactor’s nuclear chain reaction becomes self-sustaining (neither dying out nor running away). Let’s not take away from this - it’s a huge step towards demonstrating that the concept works. Note that other companies (beyond the DOE’s ten from the above announcement) have been pursuing demo units before the commercial version is built. Here is Kairos, a year ago, announcing the beginning of construction of its demo unit.

What’s happening: The core is loaded with fuel, startup tests are underway, and the control rods are adjusted until neutron production and absorption are balanced.

Purpose: It’s proof-of-physics showing the reactor can achieve steady-state fission under controlled conditions.

Status: No steam to turbines, no revenue, no customers served yet. Definitely no connection to the grid.

Operation

Definition: The reactor is producing usable thermal energy for a turbine (or process heat) at its designed output.

What’s happening: Coolant loops are running at rated temperatures, turbines are spinning, and electricity (or heat) is flowing to an end user.

Purpose: Deliver the product, whether that’s power to the grid, steam to an industrial process, or heat for hydrogen production.

Status: This requires more systems to be commissioned, including steam generators, condensers, grid interconnect, safety systems, and more licensing approvals. Don’t forget the supply chain!

Why the Gap Exists

Between first criticality and commercial operation, there’s a commissioning phase that can run from months to over a year. We have not built any SMRs or advanced reactors yet, so I can’t project the actual timeline.

In SMRs, this gap could be shorter if designs are simpler, but first-of-a-kind builds will almost certainly have extended post-criticality testing.

Bottom line: The Bloomberg projection and DOE’s pilot program just put nuclear—especially SMRs—squarely in the spotlight. The opportunity is real, but so are the limits. If we want to be in the race, we have to start running now.

The future SMRs and microreactors will be mostly impacted by supply chains and the manner they are built. It seems vendors will actually be building them more like "easy little AP1000".